Victor Fonseca, Senior Associate, Real Estate at GRESB dives into embodied carbon, what it is, why it matters, and 2025 insights from the GRESB Real Estate Benchmark.

What is embodied carbon?

Embodied carbon refers to the greenhouse gas (GHG) emissions, measured in carbon dioxide equivalents (CO₂e), associated with materials and construction processes throughout a building’s lifecycle.

The built environment generates 42% of annual global GHG emissions, with 27% coming from operations of buildings and 15% coming from building materials and construction processes (i.e., embodied carbon). Embodied carbon emissions are expected to become more representative of the annual global GHG emissions from the real estate sector over time as operational energy efficiency increases and local grid decarbonization drive reductions in operational emissions.

According to Architecture 2030, an independent non-profit organization, the global building stock is expected to grow by 241 billion square meters, from 2020 to 2060, to accommodate the largest wave of urban growth in human history. This is the equivalent of adding an entire New York City to the world every month for 40 years.

Breaking down embodied carbon

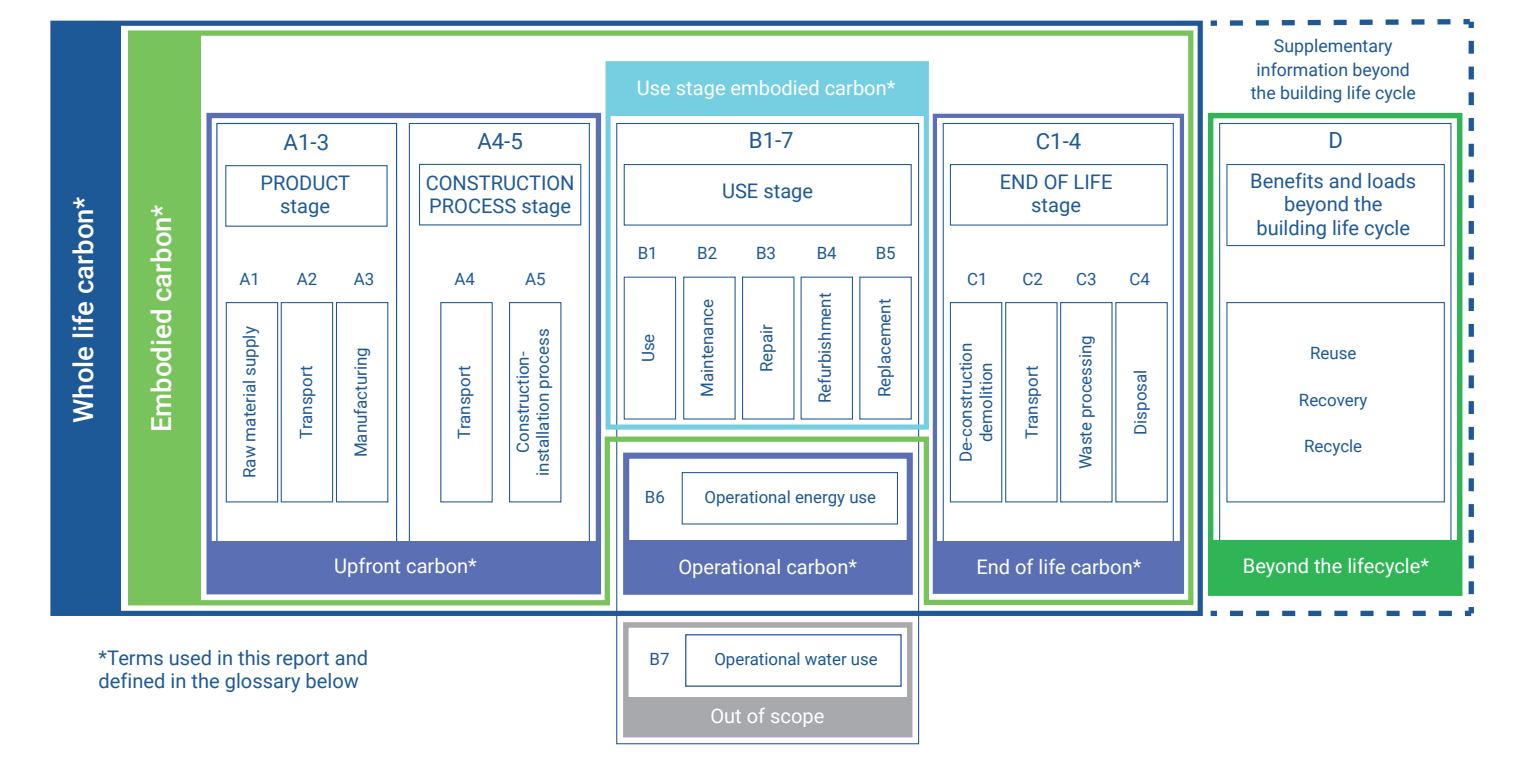

These emissions occur throughout different lifecycle stages of a building, as illustrated in the image below.

Source: WorldGBC

** Please note that B4, “Refurbishment,” and B5, “Replacement,” have been inverted in the original WGBC publication and in the above image.

The correct stages are: B4, “Replacement,” followed by B5, “Refurbishment.”

Embodied carbon, therefore, includes upfront, use stage (excluding modules B6 and B7), and end-of-life emissions as represented in the image above from the World Green Building Council (WorldGBC) report “Bringing embodied carbon upfront.”

Upfront embodied carbon

Upfront embodied carbon refers to emissions from the construction and/or major renovation of buildings. These emissions are related to materials production (modules A1–A3), transportation to site (A4), and construction-installation processes (A5), and they represent the biggest portion of embodied carbon emissions throughout the whole life cycle of a building.

This subset of embodied carbon emissions is most material for development activities, as upfront carbon is ‘locked-in’ from the moment construction works are completed and cannot be reverted. However, understanding the upfront emissions associated with the usage of the material can guide future decisions in standing investment portfolios – such as whether to renovate or demolish an asset or how to better dispose of building elements. These informed choices can help reduce future downstream embodied carbon emissions (e.g., reusing and recycling materials).

Use-stage and end-of-life embodied carbon

Use-stage and end-of-life embodied carbon are downstream emissions and occur from the practical completion of a building. These emissions are related to materials and processes for maintaining the building during the use-stage and end-of-life treatment of building elements/materials after its use (identified in modules B1–B5 and C1–C4). Modules B6 and B7 are operational emissions and are therefore not considered as downstream embodied carbon emissions.

Downstream embodied carbon is material to both development and standing investment portfolios.

More than construction

In addition, it is important to note that embodied carbon goes beyond construction. Tenants turnover and the resulting embodied carbon emitted in those fit-out works, along with the need to maintain, replace, and repair building materials throughout the entire lifespan of an asset will accumulate over time to be a significant portion of a building’s total carbon footprint. This highlights the need for these emissions to also be included in the agenda of standing investment portfolio managers.

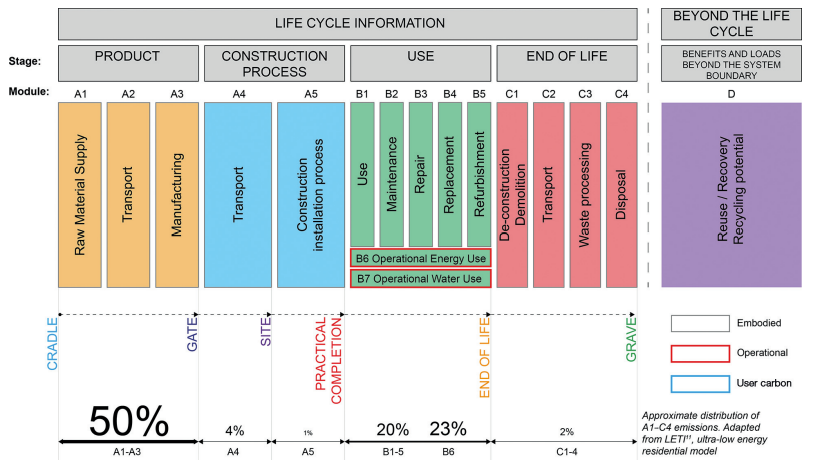

Moreover, buildings usually change ownership throughout their lifespan. This marks the need to establish rules for embodied carbon inheritance and to encourage the inclusion of embodied carbon in the due diligence risk assessment of new acquisitions. To illustrate this, the Institute of Structural Engineers breaks down the embodied carbon footprint of a building throughout different lifecycle stages. Note that not only do different lifecycle modules of embodied carbon apply to development and standing investment portfolios, but also that the magnitude of their impacts can vary significantly.

Embodied carbon in the 2025 GRESB Real Estate Assessment and beyond

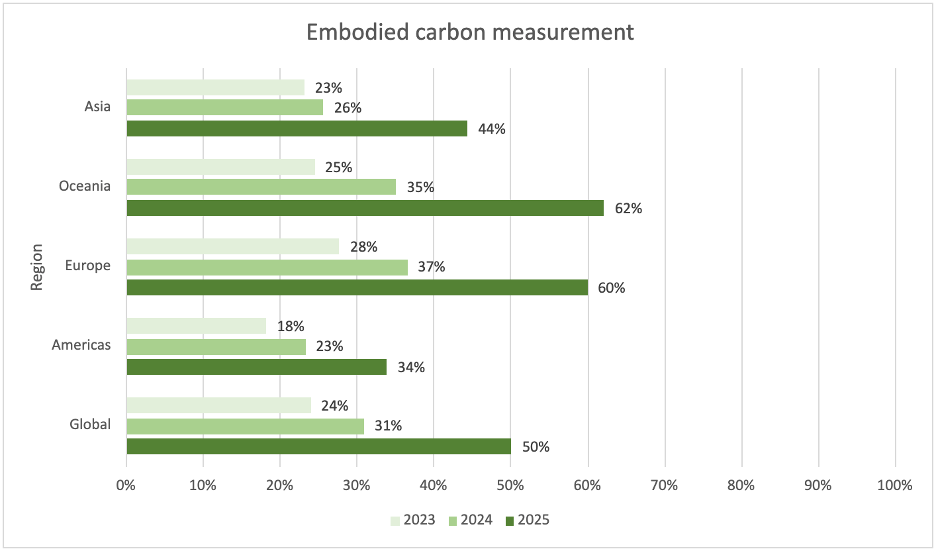

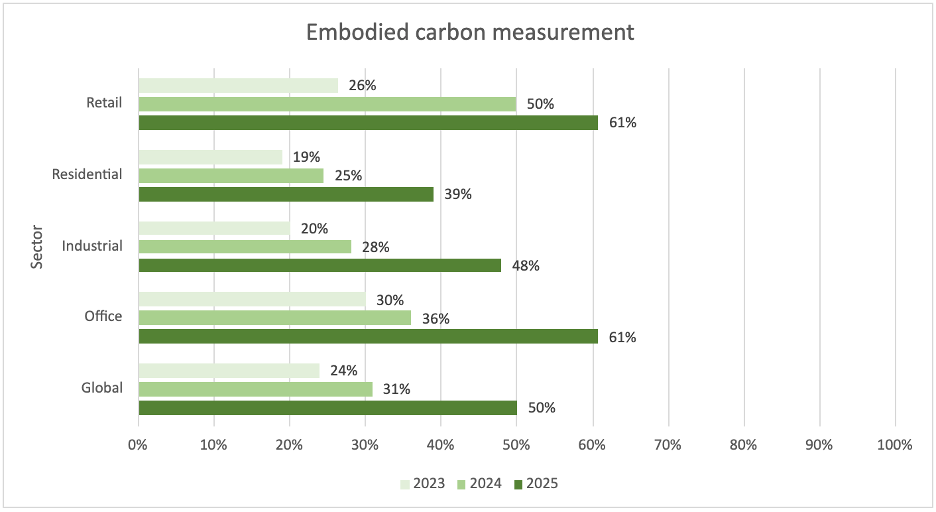

In the 2025 GRESB Real Estate Assessment, embodied carbon measurement has reached a significant milestone. Half (50%) of all development participants now report measuring embodied carbon emissions from new construction assets and major renovation projects, signaling a step change in market adoption. This represents a clear acceleration from past response rates of 31% in 2024 and 24% in 2023, following the introduction of the indicator in 2023.

Note: This measurement encompasses the A1–A5 life cycle stages and all relevant building layers.

Embodied carbon measurement continues to be shaped by regional context and asset type. Differences in data availability, existence of regulatory frameworks, and market readiness influence regional adoption rates, while sector-specific construction practices affect the feasibility of measurement. As a result, variation across regions and sectors is expected.

GRESB data highlights Europe and Oceania as regional leaders, with measurement rates more than doubling since 2023. At the sector level, office and retail assets continue to demonstrate stronger practices, with office assets showing a marked increase in measurement in 2025 and effectively closing the gap with retail, which initially led adoption.

It is important to note that these insights are directly influenced by the sample size.

Regional breakdown of embodied carbon

Sectoral breakdown of embodied carbon

This increase underscores the growing importance and recognition of embodied carbon across the real estate industry and provides clear market validation for the continued development of embodied carbon content within the GRESB Real Estate Standard, supporting action and impact.

Beyond 2025, further updates to embodied carbon are planned within the Real Estate Standard. In 2026, the non-scored embodied carbon elements developed in 2024 will be scored for the first time. In line with the Standard’s strategic direction toward performance-based scoring, the GRESB Foundation has approved a shift from portfolio-level to asset-level reporting for upfront carbon emissions starting from 2027. This change is intended to ensure that quantitative measurements are assessed within their appropriate context (e.g., sector, location), enabling more accurate performance evaluation and reward in future versions of the Standard.

Scoring and content will continue to evolve beyond 2028 to support this transition, strengthen incentives for measurement, and advance data quality. Embodied carbon is expected to remain a high-priority topic for development in the GRESB Standards and, as a result, it is likely to continue to be a key focus area for both the GRESB Foundation and the real estate sector.

Embodied carbon insights

Explore a curated collection of articles and insights from GRESB and our Partners on the critical issue of embodied carbon below. These resources provide valuable perspectives on how the industry is addressing this challenge and highlight best practices, innovative solutions, and the latest thought leadership on reducing embodied carbon in the built environment.

For more insights from GRESB, watch a short video explaining why embodied carbon is rapidly moving up the agenda and why now is the time to measure and act, and listen to our Pulse episode: “Hidden in plain sight: understanding embodied carbon for real estate.”

Thinking outside the (operational) box: The missing piece of embodied carbon

Establishing an embodied carbon strategy in the EU market

Embodied carbon in focus: Navigating investor and industry expectations

Confronting embodied carbon’s data problem: How do we know where we stand?