Water is Impact Investing

Impact investment conferences and media have begun to attract main stream investors as sponsors and participants often echoing the theme that, in our collective foolishness, we have allowed capitalism to maim our world – off balance sheet. This is a great step forward. However, the discussion often struggles to define clearly what may or may not be “Impact” and the differences and prioritization between Impact, SRI, and ESG. While grant making can help on the margin, real solutions to the destructive effects of climate change require significant impact-oriented balance sheet commitment.

Of all impact investment strategies, investing in companies and assets that deliver safe, clean, reliable water cuts through the clutter and delivers an ideal combination of market returns from free enterprises serving the common good that also deliver measurable positive impact. Making clean reliable water – also makes positive returns and impact.

We often ask Impact, ESG, SRI, and otherwise “responsible” investors the leading question; “Why is climate change bad?” Try it. You’ll find the answers often vary widely. Cutting through it all, the fact of the matter is that the main negative effect of increased carbon emissions, which is warming our planet, is on the hydrological cycle – increasing the incidence and intensifying the severity of drought and flood. In other words, climate change is primarily a water problem. Fortunately, every water problem has an investable water solution. Investors need to focus on water solutions as much as on reducing greenhouse gas emissions. No other single investment strategy can solve 15 of the 17 U.N. Sustainable Development Goals (SDGs). Investing in companies and assets that ensure a clean and reliable supply of water and sanitation does just that.

Water: a global opportunity with three distinct segments

- Water Utilities:

Water treatment and distribution utility infrastructure provides water and wastewater services to hundreds of millions of customers in their respective locales worldwide. Most operate as regulated monopolies or long term concession business models which provide for high visibility long term inflation protected cash flows, and dividends that grow steadily over time.

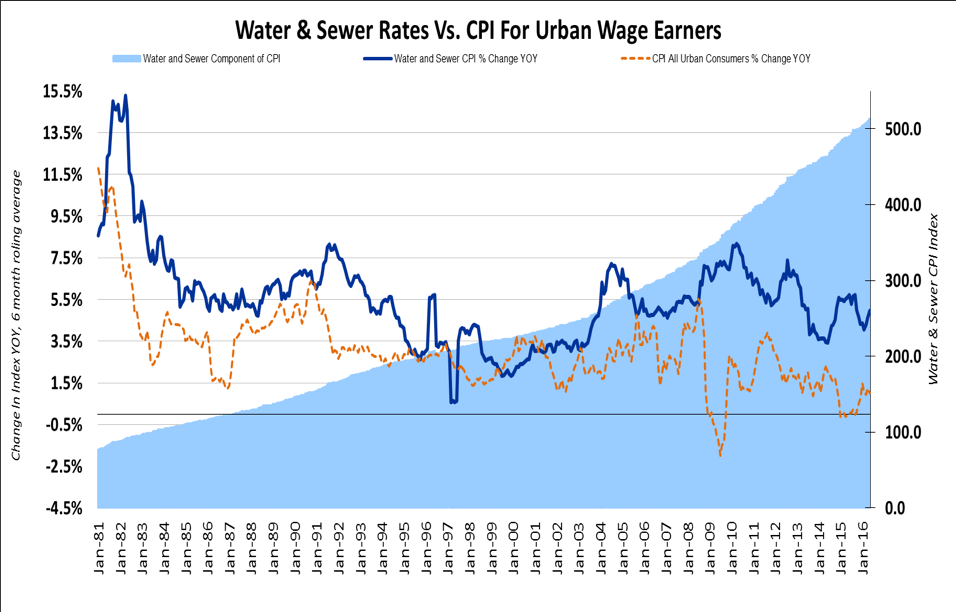

There are two common investment threads that make water utilities good long-term investments. First, water distribution utilities are regulated monopolies, which operate under a set rate of return on invested capital business model. This means that for every Dollar, Pound, Euro, or Real that a water utility invests, they typically earn a return on equity ~ 9% – 10%. Second, water utilities are, typically, allowed to increase their water tariffs to rate payers, at least in-line with inflation (as measured by CPI in most countries and RPI index in U.K.). This means the companies have uniquely strong pricing power, and as illustrated by the chart below (using U.S. as an example), water and sewer rates have historically exceeded CPI, thus offering investors inflation-protected returns.

As a result, water utilities generate highly visible, inflation protected, EPS and dividend growth, typically averaging 5% – 7% annually. Water utilities also pay out annual cash dividend yields through thick and thin – currently averaging > 3%.

Water utilities can also be excellent environmental stewards. Recently, Water Asset Management (WAM) conducted a survey among some of the largest listed water utilities globally. Along with measuring quantities of water delivered, customers served, and waste water treated, we also surveyed annual greenhouse gas (GHG) emissions from water and wastewater treatment plants. We found that, collectively, these large global water utilities have reduced GHG emissions from their portfolio by ~5% over the last five years. Additionally, water utilities are also generating more of their power from self-generated renewable resources. Case in point is a U.K. based listed water utility, Severn Trent, currently generating almost a third of their power from renewable resources with ambitions to reach 50% over the next several years.

Transparent, progressive regulatory models governing water utilities make them a win-win business model for shareholders, customers, and the environment. WAM has a team focused on our investment universe of listed utilities in the U.S., Latin America (Brazil and Chile), U.K., Continental Europe (Italy, France, and Greece), as well as Asia including China and Philippines. We also have a separate specialized team focused on the Private Equity water infrastructure investment opportunity in the U.S., which we describe as the world’s biggest emerging market opportunity, with TLC; transparency, rule of law, and regulatory certainty.

- Water Infrastructure & Technology Companies

These companies provide the ‘back-bone’ for water services, worldwide, including water pumps, pipes, valves, irrigation equipment, fire hydrants, water heaters, water meters, leak detection, water treatment, irrigation, water quality data and analytics, and various other water related equipment and products. Inherent in these business models are products and solutions that ultimately save water, treat water, or move water using less energy.

Importantly, many of these water infrastructure companies are selling more environmentally friendly products and solutions because there is an economic payback for customers to buy more sustainable products. Examples:

- Pump companies with new pumps that reduce emissions by 90% and fuel consumption by 10%.

- Manufacturer of drip irrigation that helps farmers save 30-65% of the water used in traditional surface irrigation systems.

- Global water and sanitation services companies that have helped customers conserve 171 billion gallons of water annually through innovative product offerings that reduce labor time and water usage while increasing performance.

Like most other industries, many water infrastructure companies are still in the process of gathering ESG related metrics and data and we are encouraged by the increasing number of water companies willing to disclose relevant ESG metrics.

From an investment standpoint, the investment characteristics of water companies are very attractive. Many operate as unregulated oligopolies which enables strong pricing power. Additionally, large installed bases mean recurring revenues often exceed new installation sales. Free cash flow yields in the mid single digits along with healthy balance sheets allows for capital allocation flexibility for enhanced dividends, share repurchases and smart M&A. Finally, strong operating cultures allow for mid-teens type earnings growth in a steady, moderate growth economic environment.

- Water Resources: The Sustainable, Perpetual, Real Asset

WAM collaborates with local farmers to bring enhanced water consumption efficiencies to specific water-rich farms located in the desert south western U.S. with adjudicated water rights. We then utilize proven, century old, market mechanisms to provide long term, reliable supplies for communities in that region’s $5 trillion economy seeking to enhance the reliability of their long term water supplies. Water rights are the original cap and trade business model, established more than 100 years ago. First, an aquifer or river’s recharge rate was calculated, then, consumptive use was quantified at less than the recharge rate. That amount of consumptive use was allocated to individual water rights holders, and those water rights can be traded or leased like any other form of real property. Unlike most other real assets, there is no depletion curve on a water right; it functions in perpetuity.

Water Is Impact

As we all know, water is life. Water is also impact. Many water companies and related assets as described above are also perpetual. Water is non fungible and cannot be replaced by something else. It’s difficult for long term, real asset investors to make the same claim for many other infrastructure business models which may face negative demand from long term disintermediation driven by technology, innovation, and changing global trade practices. Clean water is scarce and its price should continue to go up. That stands in stark contrast to energy, where pricing faces downward pressure. Water is impact and will provide great opportunities for decades to come for those seeking the potential for superior risk adjusted returns.

This article is written by Matthew J. Diserio Co-Founder and President at Water Asset Management, LLC.