The importance of Scope 3 emissions

Scope 3 emissions—those occurring in a company’s value chain, both upstream and downstream—represent a significant share of total emissions for infrastructure assets. According to CDP, the Scope 3 emissions of a company are often several times greater than its Scope 1 and 2 emissions combined, especially in sectors involving heavy procurement, construction, or use-phase emissions.

For infrastructure assets, where operations frequently rely on external suppliers, contractors, and users, understanding and managing Scope 3 emissions is essential. These emissions are critical to identifying the true carbon intensity of an asset and informing meaningful decarbonization strategies.

Why Scope 3 emissions matter to investors

From an investor perspective, Scope 3 emissions are integral to assessing the full climate impact and transition risk of infrastructure assets. Transparency and consistency in Scope 3 reporting enable investors to make informed comparisons of carbon intensity and resource efficiency of assets across portfolios.

The IIGCC highlights that despite inherent complexity, Scope 3 emissions are central to credible net-zero transition plans. Investors are increasingly looking for disclosure not just of emissions data but of the processes used to determine which Scope 3 categories are material and how these are managed.

The challenge of materiality

Most major climate frameworks—including the GHG Protocol, TCFD, and various regulatory schemes—require reporting and target-setting across Scope 1, 2, and material Scope 3 emissions. The challenge lies in the word “material”: what constitutes material Scope 3 emissions can vary significantly between, and even within, sectors.

The difficulty is compounded in infrastructure, where similar assets may differ in business models, ownership of equipment, or operational boundaries. For example, two airports may vary in whether they own or outsource ground handling services, affecting their Scope 3 profile.

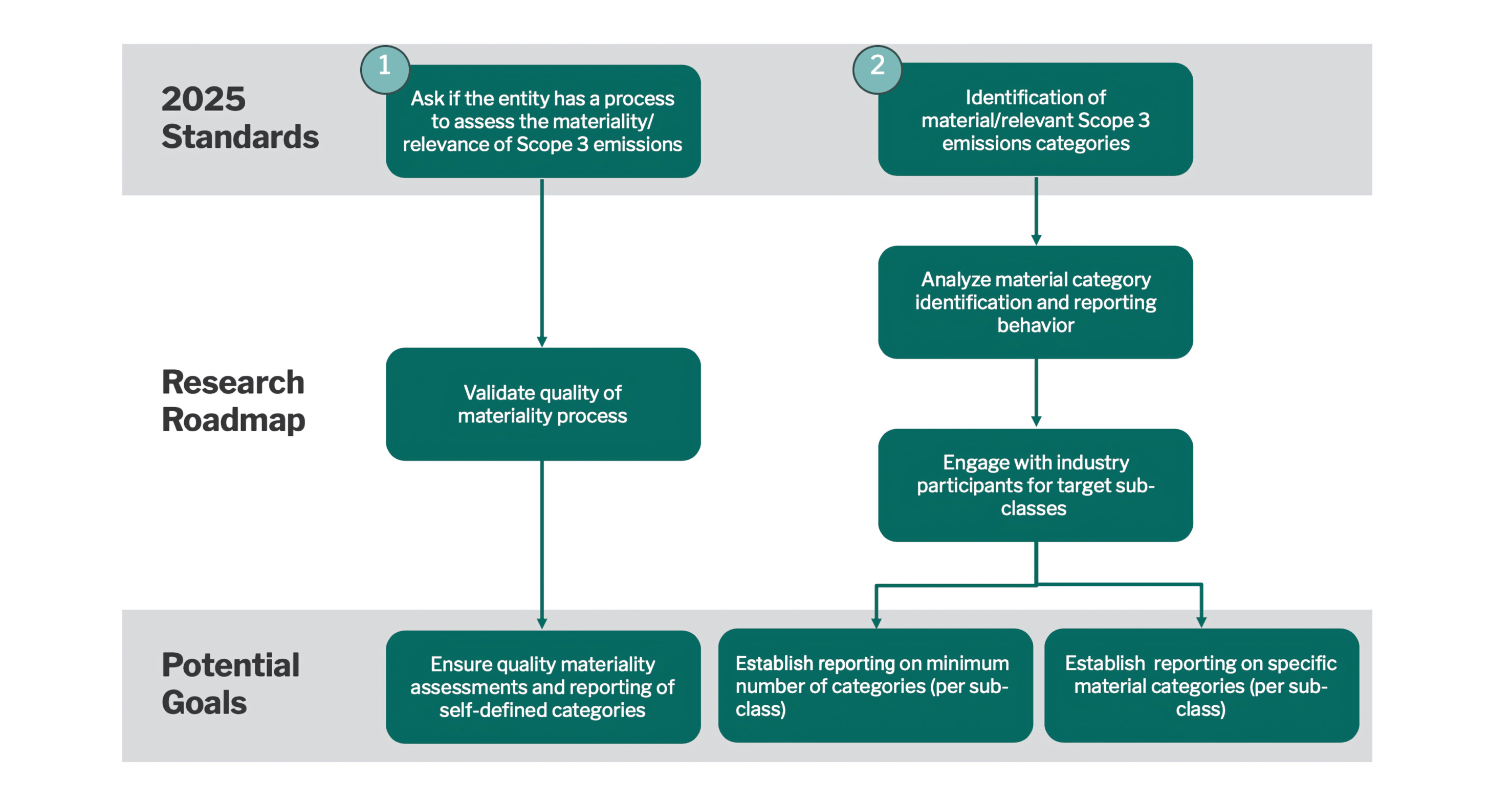

While sector-level guidance exists, such guidance is often not sufficient to promote consistent benchmarking. Given the size of the GRESB infrastructure asset universe, the diversity of sectors represented, and the standardized nature of its data collection process, GRESB is uniquely positioned to leverage its platform in two key ways: first, to research how materiality is defined and how Scope 3 emissions are currently reported across different assets; and second, to develop best-practice guidance that enhances industry-wide practices and strengthens the role of Scope 3 emissions in driving net-zero transitions.

What the data shows

To better understand how Scope 3 emissions are identified and reported, GRESB conducted a targeted survey of infrastructure asset participants. The results revealed several key insights:

- Diverse reporting on Scope 3 categories: There was significant variation in the number and type of Scope 3 categories reported. In many cases, categories identified as material were not actually reported in the 2024 Assessment.

- No universally material categories: No single Scope 3 category was considered material across all participants within any infrastructure sub-sector. This makes it difficult to mandate a standard set of Scope 3 categories even at the sub-sector level.

- Discrepancies between materiality and reporting: Survey data showed mismatches between categories flagged as material and those reported in the assessment, suggesting a lack of alignment between perceived importance and disclosure practices.

- Uncertainty in materiality assessments: A significant number of respondents had not conducted a formal materiality assessment but still provided views on which Scope 3 categories were relevant, raising questions about the confidence and consistency of these determinations.

These findings suggest that it is premature to mandate reporting of specific Scope 3 categories by sector. Moreover, the current flexibility in GRESB’s reporting structure does not allow users to distinguish between material and non-material Scope 3 disclosures. This limits the comparability and utility of reported data. Finally, there remains a gap in the quality and consistency of procedures used to assess and determine which Scope 3 emissions are material and how they are estimated.

GRESB’s forward-looking approach

GRESB is taking a two-pronged, data-driven approach to address the challenges of Scope 3 reporting and materiality:

- Focus on process quality: GRESB asks whether a process exists for assessing the materiality of Scope 3 emissions. If so, participants are requested to describe it. This information allows for research into what constitutes a robust materiality assessment and helps identify common elements that could form the basis for minimum expectations. This also enables further analysis of how identified material categories relate to the quality of the underlying materiality assessment processes.

- Increased transparency: Participants are now asked to identify which Scope 3 categories they consider material. This disclosure will not affect scoring and is not intended to influence reporting behavior. Rather, it enhances transparency and enables more informed use of reported data.

Conclusion

GRESB recognizes that Scope 3 emissions are both vital and complex. Rather than attempting to prematurely standardize Scope 3 reporting, GRESB is taking a measured, research-based approach. By enhancing transparency around materiality assessments and collecting structured data on reported categories, GRESB is laying the groundwork for more meaningful, comparable, and credible Scope 3 disclosures, driving progress toward better sustainability performance and investment decision-making.