NYISO Contemplates Carbon Pricing – How Much Will Rates Increase?

Published on 4 Oct 2017

New York State’s goals are to reduce economy-wide (not just electricity sector) greenhouse gas (GHG) emissions 40% from 1990 levels by 2030 and 80% by 2050. Over the past year, the implementation of TOTS, CES, and ZECs, as well as the value stack rate design and REV, have moved the State closer to achieving its carbon policy objectives. However, the wholesale electricity market is not aligned with the State’s aggressive decarbonization goal. As such, the NYISO asked the Brattle Group to evaluate how carbon pricing can be incorporated within wholesale markets, and their findings were released in a report last week. If implemented, electricity rates for all customers will increase, but by how much? Read on to find out the potential impact on electricity rates.

Why carbon pricing?

Don’t we have CES, ZECs, and RECs?

How will it work?

What will be the impact on electricity rates?

When will carbon pricing be implemented?

(Summary below paraphrased from the Brattle Group report Pricing Carbon into NYISO’s Wholesale Energy Market to Support New York’s Decarbonization Goals)

WHY CARBON PRICING?

Presently, the wholesale electricity markets operated by NYISO are not aligned with the state’s decarbonization objective. The wholesale markets are designed to provide electricity reliably and cost effectively, but the costs considered in the markets do not include the cost of carbon emissions—except as conveyed through the RGGI price, which is currently quite low. By not internalizing the environmental costs, the markets are not aligned with New York’s carbon reduction targets. This inconsistency is growing as carbon policy objectives become more ambitious. The state’s goals are to reduce economy-wide greenhouse gas (GHG) emissions 40% from 1990 levels by 2030 and 80% by 2050.

DON’T WE HAVE CES, ZECS, AND RECS?

Carbon pricing would invite a broader, more competitive range of solutions than targeted procurements under the CES alone. Higher carbon prices would provide a stronger market signal than current RGGI prices and reward efficiency improvements across the fossil fleet, incentivize conservation and energy efficiency, encourage storage and other technologies that can reduce emissions, and lead to other market responses that are difficult to predict. Reducing electricity emissions by 40% or implementing the CES alone will be insufficient by itself to meet the 40% economy-wide emissions reduction goal. Decarbonizing enough to accomplish economy-wide goals will likely require significant electrification of transportation and space heating (with heat pumps), end-use efficiency, and disproportionate emissions reductions in the electricity sector by 2030.

CES procurement of RECs and ZECs does not invite competition as broadly as carbon pricing would since it targets specific resource types and amounts dependent on solicitations from New York State Energy Research and Development Authority (NYSERDA). The CES further differs from a pure carbon price approach in that it does not price the externality directly, but rather acts as a proxy for carbon. It is an imperfect proxy that is constructed as if all clean generation displaced the same amount of carbon no matter when or where it is produced.

HOW WILL IT WORK?

There are three options reviewed in the Brattle Group analysis – carbon charge, cap-and-trade, and tightening the existing RGGI cap to increase carbon prices.

The first option, a carbon charge, directly sets a $/ton price on carbon emissions, which NYISO would apply in its commitment, dispatch, and settlement. The carbon charge approach would recognize the cost of carbon emissions from all power sector emitters, directly internalizing the environmental externalities. NYISO would administer the carbon charge in its commitment, dispatch, and settlement processes. NYISO would add the charge to the commitment and dispatch cost of New York’s fossil-fired generators based on each generator’s emissions rate, and then deduct that amount from the generator’s compensation payment for its energy.

The second option, cap-and-trade, would establish a cap on emissions by issuing or auctioning a limited number of allowances. Developing a state-specific cap-and-trade program would impose an administrative burden for design, operation, and compliance. The state would need to designate an entity (or entities) to design and administer the program. This entity would need to develop operating rules, including price control mechanisms and allowance allocations.

A third approach is to tighten the existing RGGI cap to increase carbon prices. Because RGGI is a regional program, RGGI states would have to agree to tighten the RGGI standard. This could be the best approach if the region shares common goals, but each state does not share common goals.

Of the three approaches, a carbon charge would likely be the best approach. A carbon charge would likely incentivize the following types of operational and investment changes to abate emissions at a cost at or below the price of carbon:

Shifting unit commitment and dispatch to ward lower-emitting existing resources.

Tilting investment in renewable resources (procured under CES using Tier 1 RECs)toward those that generate at the times and places that displace the most carbon.

Supporting investment in new, efficient gas-fired combined cycle generation that can displace higher-emitting existing generation and imports.

Supporting investment and operation of distributed energy resources, including storage and demand response.

Promoting energy efficiency through higher per-kWh charges, even if demand charges, customer charges, or overall customer costs decrease.

Encouraging other innovative solutions and idiosyncratic decarbonization opportunities that are difficult to imagine today.

WHAT WILL BE THE IMPACT ON ELECTRICITY RATES?

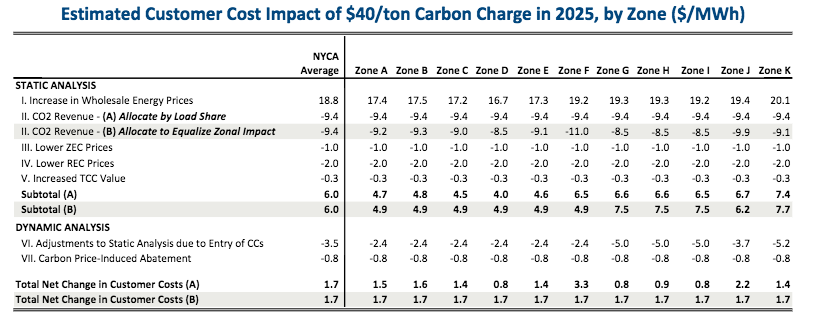

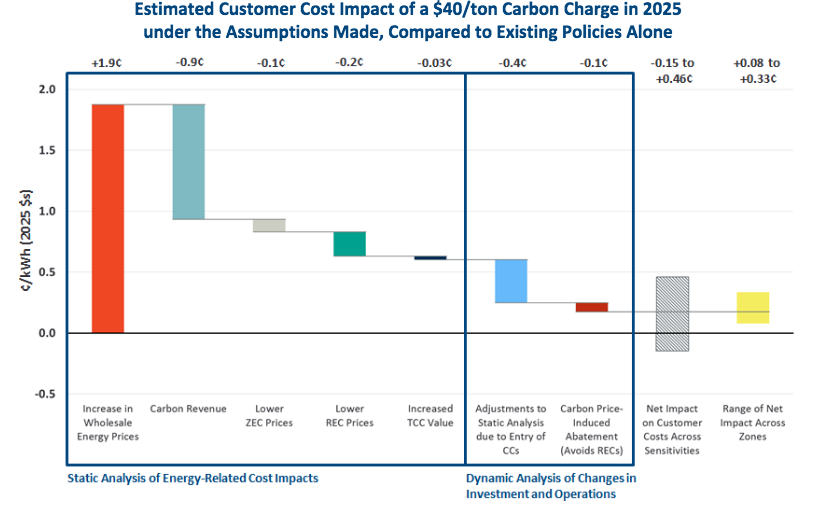

If carbon pricing is implemented, the projected impact ranges from $.008/kWh to $.033/kWh, depending on the pricing zone. Or, if costs are allocated to equalize the impact across zones, the increase is rates is projected to be $.017/kWh.

Although average wholesale energy prices would increase by about $.019/kWh, about 50% of the cost could be offset by returning carbon revenues to customers; another 18% would be offset by reduced prices for RECs and ZECs in the presence of higher wholesale energy prices, and increased TCC revenues; finally, another 23% would be offset by dynamic effects on investment signals.

WHEN WILL CARBON PRICING BE IMPLEMENTED?

Carbon pricing may or may not actually be implemented. The NYISO asked the Brattle Group to examine the potential for using carbon pricing within wholesale markets to further New York’s energy goals, with the first step being the publication of this report. Next, the NYISO and DPS will jointly convene a one‐day conference on September 6, 2017 where all interested stakeholders will have the opportunity to hear from, and present questions to, the authors of the Brattle study and staff from DPS and the NYISO. Details about the location and agenda for this conference will be forthcoming in a few weeks. Stakeholders are invited to contribute to the development of the agenda by submitting questions concerning the report to [email protected] by September 1, 2017.

This article originally posted on the EnergyWatch website. Sources:

Newell, S. A., Lueken, Weiss, Spees, Donohoo-Vallett, & Lee. (2017, August 10). Pricing Carbon into NYISO’s Wholesale Energy Market to Support New York’s Decarbonization Goals. Retrieved August 14, 2017, from https://www.nyiso.com/public/webdocs/markets_operations/documents/Studies_and_Reports/Studies/Market_Studies/Pricing_Carbon_into_NYISOs_Wholesale_Energy_Market.pdf?_cldee=YW5keUBlbmVyZ3l3YXRjaC1pbmMuY29t&recipientid=contact-df9fd602d0eae4119401005056815c52-d11c9c33469c47f381f60c4ced3afd0e&esid=b19eeb95-c17e-e711-9435-005056815c52

Related insights

Articles

Energy Security through Sustainable Supply Chains

Energy security is the availability, accessibility, affordability, and acceptability of a sustainable energy supply. This is a key sustainability issue as demonstrated through the Sustainable Development Goal 7 to “ensure access to affordable, reliable, sustainable and modern energy for all”.

The internet is big, and it is growing bigger. This is what happens on the internet every 60 seconds, and it is but a tiny snapshot of everything that happens. Our digital lives are becoming increasingly dependent on this network, but this is having an increasing physical impact too. Alongside the visible infrastructure that crisscross […]

2019 will be the year of adaptation to climate change: the French perspective

Decreasing energy consumption (of buildings in particular) is one of the major priorities of energy and climate policy in France following the Paris Agreement in 2015. This decrease considers all activity areas, especially real estate, which accounts for a large share of French carbon emissions (27%). With its first “Low Carbon National Strategy”, France is […]