The Gulf Cooperation Council (GCC) real estate market is experiencing a significant ESG shift. The three main driving forces include: stock exchanges introducing disclosure requirements, institutional investors routinely requesting performance data, and climate regulations that are starting to demand emissions accounting.

The proliferation of new requirements reflects a growing census among standard-setting bodies and national governments: sustainability information is a material consideration for institutional investors. For example, in 2023, the GCC Exchanges Committee’s unified ESG metrics explicitly reference GRI Standards. The UAE Climate Decree-Law (11) specifies GHG Protocol for emissions and Saudi Vision 2030 aligns with the same international frameworks. Standardized ESG metrics are becoming the common language for regional real estate.

Regulatory trends

GCC stock exchanges have introduced sustainability disclosure frameworks at varying levels of maturity and adoption. The GCC Exchanges Committee published unified ESG metrics in 2023, drawing heavily on GRI standards and encouraging Sustainable Development Goal (SDG) alignment. UAE’s ADX and DFM mandate annual sustainability reports for listed companies, Saudi Tadawul requires disclosures aligned with Vision 2030, while Bahrain, Qatar, Kuwait, and Oman maintain voluntary guidelines.

Beyond listed company requirements, the recent UAE Federal Decree-Law (11) on climate change establishes emissions reporting obligations across sectors, including real estate, setting a precedent in the region. While there is a clear direction, actual reporting remains in early stages and, where it does occur, the comparability of metrics and methodologies is limited across portfolios. This reflects differences in choices made by individual firms about emissions boundaries, data collection methods, and reporting time periods.

Investor pressure and capital access

International institutional investors and regional sovereign wealth funds now routinely request sustainability performance data during due diligence assessments. Corporate tenants, especially multinationals operating across the region, increasingly require the same. These stakeholders want comparable metrics that demonstrate how an asset or portfolio performs against peers.

Without standardized benchmarking, assets require bespoke evaluation when competing for international capital. Additionally, there is risk of greenwashing as well as greenhushing, both of which structured benchmarking helps mitigate.

The distinction matters: certifications verify design or operational attributes at a point in time, while benchmarking evaluates portfolio-wide performance and improvement trajectories over multiple years. Individual building certifications provide asset-level credentials but lack the comparative context, tracking over time, and portfolio-level insights that investors and institutional capital require. Portfolio-level benchmarking provides this comparative and longitudinal context.

Why benchmarking matters

Benchmarking offers tangible value: asset-level data across energy, water, and waste identifies specific efficiency opportunities, and portfolio-level aggregation reveals patterns that individual asset reviews miss. Organizations managing sustainability through integrated benchmarking avoid duplicated consultant engagements across portfolios, redundant data collection, and inconsistent methodologies across multiple reporting requirements.

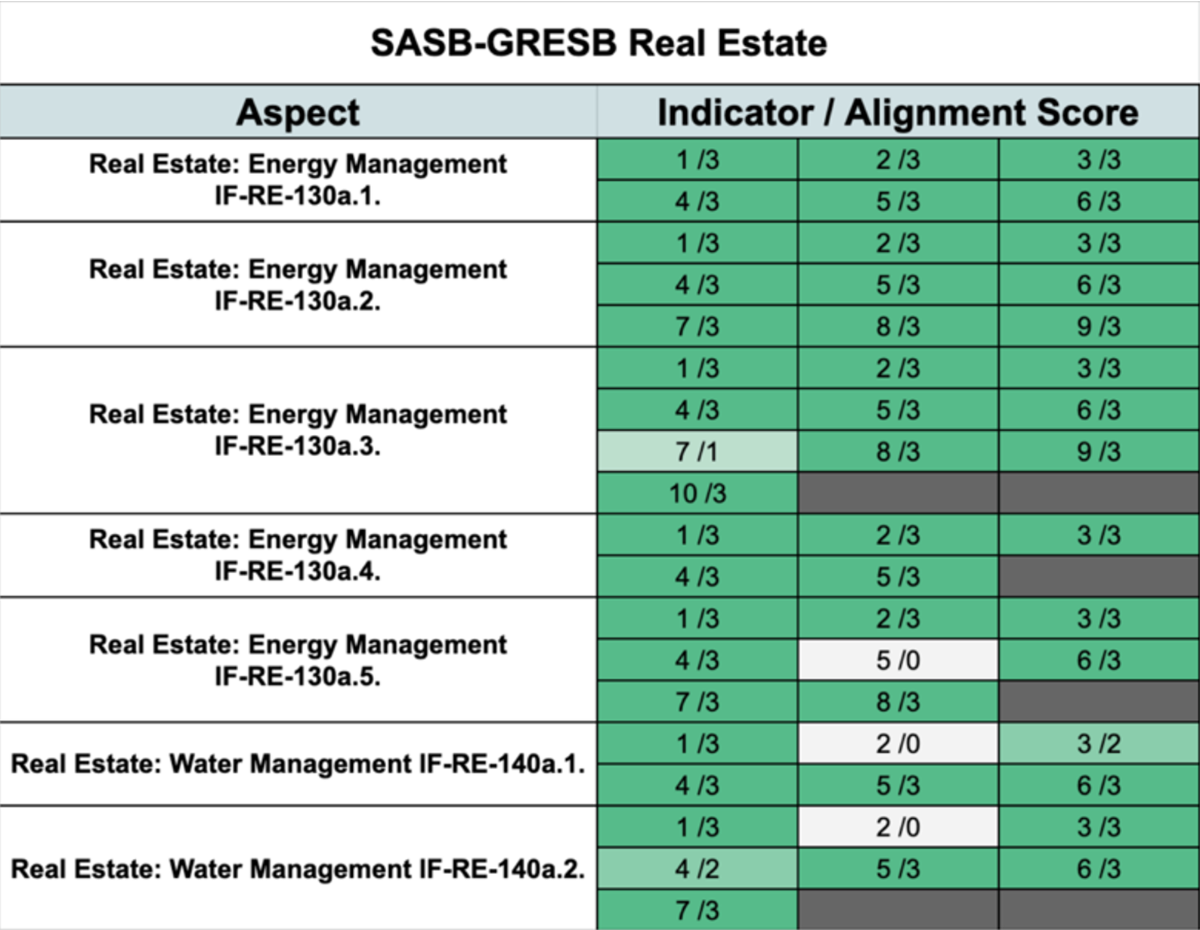

GRESB, as the global sustainability benchmark for real assets investments, aligns with frameworks including GRI, TCFD, and CDP. GRESB explicitly recognizes and integrates green building certifications, including both new construction and operating schemes (e.g., . LEED, Estidama, and GSAS). GRESB is well-aligned with the Sustainable Account Standard Board (SASB) criteria underpinning International Sustainability Standard Board (ISSB) guidance. A recent crosswalk shows that GRESB meets 80% of SASB disclosure criteria, and SASB indicates that its requirements will recognize future versions of GRESB as definitive.

Organizations can use the same underlying data for multiple disclosure requirements, maximizing return on the effort invested in measurement.

Additional information about common GRESB crosswalks is available here.

GRESB evolution

Recent updates to the GRESB Real Estate Standard help address some of the challenges facing GCC participants. One example is the incorporation of absolute energy efficiency thresholds with climate zone-specific performance targets. These targets, introduced in 2025, have a number of advantages:

- They reference the ASHRAE 100 Standard. The Standard is the product of a rigorous ISO/ANSI development process. It provides property- and climate zone-specific benchmarks for efficient building operations.

- GCC member states are covered by ASHRAE Zones 1B (Very Hot, Dry) and Zone 2B (Hot Dry). These are used to adjust energy use intensity targets to regional conditions.

- The ASHRAE 100 thresholds allow participants to receive recognition with only one year of performance data (as opposed to two with previous pathways).

ASHRAE’s Standard development is part of a broader program of work in partnership with the GCC Standardization Organization.

GRESB hopes to apply similar approaches to additional issues, such as emissions and water use in future Standard releases.

The case for early adoption in GCC

GCC participation in global sustainability benchmarking remains relatively limited, creating both challenge and opportunity. The challenge is sparse regional peer data. As an example, GCC portfolios operate in distinct conditions such as high cooling demands, distinct regulatory environments, and different building typologies. Without regional benchmarks, local portfolios competing for international capital lack the context to show their relative performance.

Early participants can help shape what strong performance looks like in GCC operating contexts rather than chasing benchmarks set by portfolios in different operating environments.

This matters particularly as regulatory requirements formalize. As emissions reporting requirements expand across the GCC, credible disclosure depends on consistent data structures. Portfolio-level emissions must be calculated using standardized boundaries (Scope 1, 2, and 3), consistent methodologies (e.g., GHG Protocol), and comparable metrics across reporting periods. Organizations without benchmarking infrastructure may face a steeper learning curve.

GCC leadership

The GRESB sustainability benchmark has recognized the practices and performance of a number of GCC-based companies. Examples include:

- Sobha Reality – achieved an outstanding score of 97 of 100 points in the 2025 Real Estate Assessment. This reflected a three-year transformation from a 2023 score of 73. Learn more.

- Majid Al Futtaim – demonstrated its long-term commitment to sustainability by achieving its 12th consecutive Green Star designation. In 2025, the firm was also recognized as a sector leader in non-listed, residential real estate. Learn more.

These GCC leaders illustrate the value of sustainability benchmarking. Sobha Realty used GRESB to measure, track, and communicate its improvement over time. Majid Al Futtaim demonstrated its long-term commitment, sustaining superior performance for over a decade. The firms illustrate benchmarking as a tool to communicate both leadership and improvement to their stakeholders.

GCC investor engagement

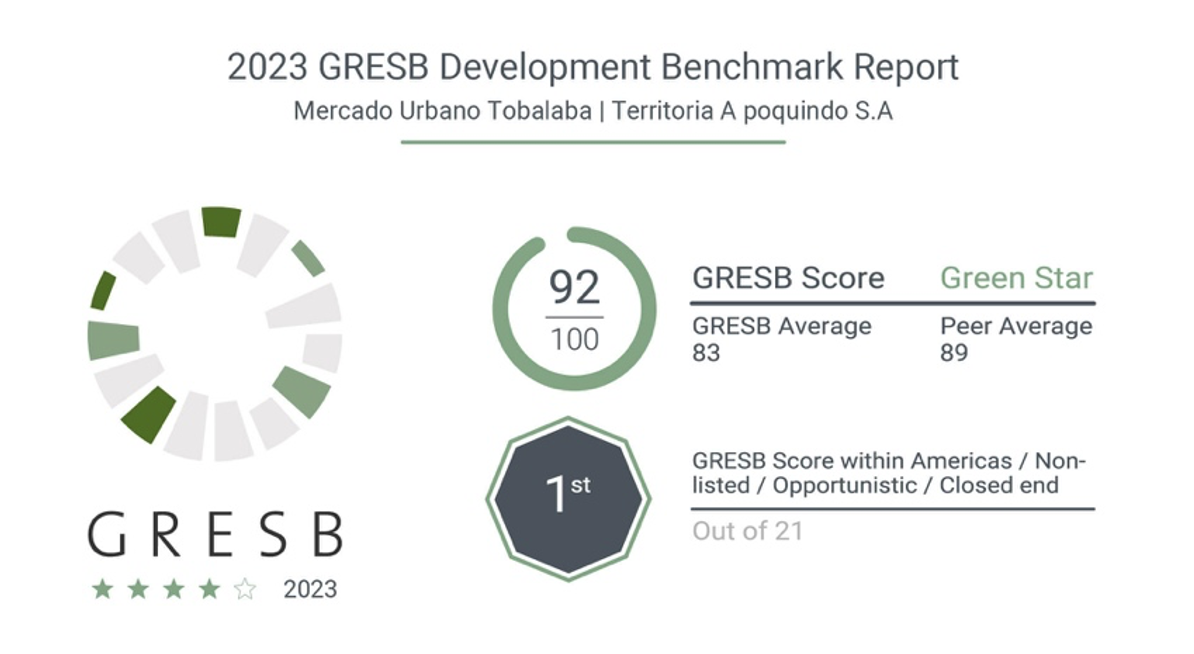

GCC-based investors have begun to create value and reduce risk by engaging on sustainability issues. One example is the Abu Dhabi Investment Authority (ADIA) investment in Territoria Apoquindo, a marquee real estate project in Santiago, Chile.

The project includes approximately 40,000 square meters of prime office and 35,000 square meters of experiential retail linked to a busy metro station. The project used GRESB to benchmark its sustainability strategy and communicate its industry leadership to ADIA. The GRESB development benchmark recognized the project’s exceptional green building activities, while also communicating its superior sustainability strategy and risk management activities. This project illustrates the role of sustainability benchmarking in protecting the value of GCC investments and communicating its leadership.

Building the infrastructure

Building robust ESG measurement infrastructure takes time: developing data collection systems, training teams, refining methodologies, and establishing baselines typically requires two to three years to fully mature. Organizations starting this work today will have operational measurement systems and multi-year performance datasets when standardized reporting becomes wide-spread practice across the GCC. In a region moving quickly on climate commitments and economic transformation, this head start matters.

References

- UAE Legislation. Federal Decree-Law No. (11) of 2024 on the Reduction of Climate Change Effects. Federal Decree-Law. 2024. https://uaelegislation.gov.ae/en/legislations/2558

- GCC Exchanges Committee (via Dubai Financial Market). GCC Exchanges Committee Unified ESG Disclosure Metrics. 10 Jan 2023. https://feeds.dfm.ae/documents/2023/Jan/10/d308a4c4-332b-441c-b1eb-13bf4adf78fe/DFM_PR_GCC%20ESG%20Metrics%20_E_10_01_2023.pdf

- Abu Dhabi Securities Exchange (ADX). ESG Disclosure Guidance for Listed Companies. Guidance (PDF). https://www.adx.ae/-/media/adx/related-documents/sustainability/esg-disclosure-guidance-for-listed-companies—english.pdf

- Saudi Exchange (Tadawul). ESG Disclosure Guidelines. Guidance page. https://www.saudiexchange.sa/wps/portal/saudiexchange/listing/issuer-guides/esg-guidelines/

- ASHRAE; GCC Standardization Organization (GSO). ASHRAE–GSO Memorandum of Understanding. 09 Jun 2024. https://www.ashrae.org/file%20library/communities/memoranda%20of%20understanding/ashrae–gso-mou_june-2024.pdf

This article was co-authored by Hussein Gubran, ESG Manager (KEO International Consultants), and Chris Pyke, Chief Innovation Officer (GRESB), with contributions from the KEO ESG team. Learn more about KEO here.

Read more from our partners.