Our industry is engaged in an important dialogue to improve the efficiency and resilience of real assets through transparency and industry collaboration. This guest article contributes to that conversation and does not necessarily reflect GRESB’s views or position, nor does it represent an endorsement. The GRESB Insights blog is designed to share diverse industry perspectives and foster informed discussion on key topics for real assets investments.

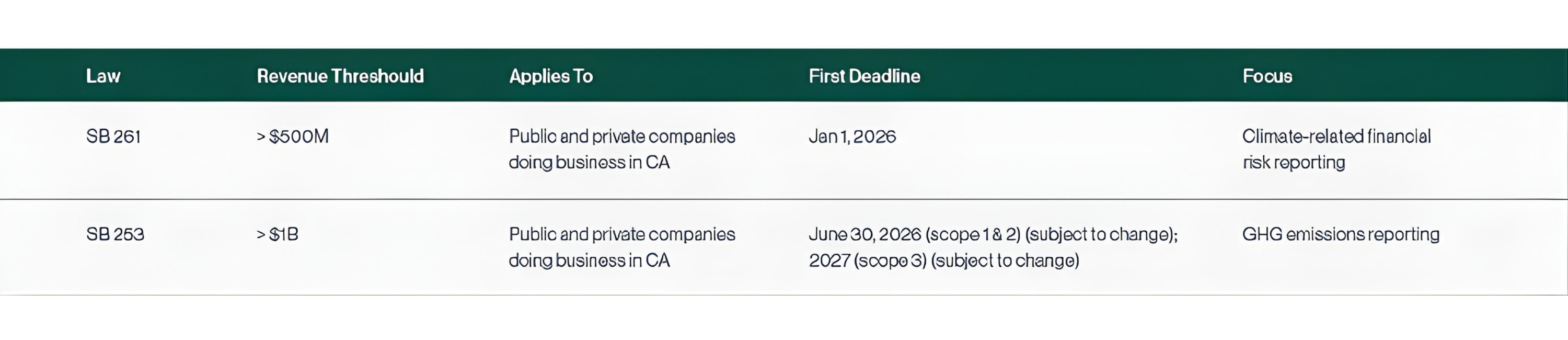

Together, California’s SB 261 and SB 253 establish the most comprehensive state-level climate reporting requirements in the nation. Adopted in 2023, SB 261 requires disclosure of climate-related financial risks, while SB 253 mandates GHG emissions reporting.

By aligning with global standards for climate transparency, California is setting the pace for U.S. disclosure—with states like New York, Illinois, Colorado, and New Jersey moving in the same direction. Designed to provide decision-useful information for investors and other stakeholders, these laws advance consistent, comparable climate reporting across markets.

The first deadline for SB 261 is January 1, 2026, and will cover all sectors, including real estate, banks, retailers, manufacturers, and other companies with California holdings or operations. Initial rulemaking is expected from the California Air Resources Board (CARB) by the first quarter of 2026, but the deadlines and core requirements of the CA climate rules are already written in law (See bill text: SB 253; SB 261).

First: See if you’re impacted

CARB’s preliminary list of covered companies (published on September 24) is a helpful starting point.

It includes over 4,000 public and private companies, along with some nonprofit organizations, that may be required to comply with SB 261 and/or SB 253. However, some expected names are missing, meaning the list should not be misconstrued as exhaustive. Companies doing business in California should confirm independently whether they are in scope.

Proposed definitions for applicability

Proposed definitions for applicability are still under review, forcing companies to move forward with compliance efforts as the industry waits for more information. So far, CARB has signaled the following:

- Revenue may be defined as gross receipts under California Revenue and Taxation Code (RTC) §25120, although CARB has also discussed alternative approaches, such as using global sales. Final guidance is pending.

- Doing business in California was initially proposed to align with the tax code definition under RTC § 23101, which includes thresholds for sales, property, or payroll (e.g., sales above USD 735,019). However, CARB has since indicated it may explore alternative approaches, and the final definition remains under review.

Applying these criteria in practice can be complex, particularly for companies with multiple subsidiaries or shared service operations, where consolidating reporting boundaries and revenue can be less straightforward. With deadlines upon us, organizations need to prepare disclosures under the assumption they will need to disclose while awaiting final applicability guidance.

To support the applicability determination, CARB also released a voluntary stakeholder survey that lets companies input business information to help determine if they are in scope of the reporting requirements.

SB 261 and climate risks: The immediate priority

Companies must prepare a public report on climate-related financial risks by January 1, 2026, to be posted on their website and aligned with accepted frameworks such as the Task Force on Climate-related Financial Disclosures (TCFD) or the International Financial Reporting Standards (IFRS) S2 Climate-related Disclosures. Reports must cover:

- Governance

- Strategy

- Risk management

- Metrics and targets

For companies new to climate-risk reporting, the challenge of building systems, collecting data, and preparing credible disclosures by the end of 2025 is steep. SB 261 reports will be public and thus may face scrutiny from customers, regulators, banks, and investors—weak or incomplete filings carry not only regulatory but also reputational risk.

CARB’s draft checklist (published on September 2) sets minimum expectations and emphasizes that disclosures should be prepared through the lens of “decision-usefulness for investors and other stakeholders.” Importantly, it clarifies that GHG emissions are not required to be reported under SB 261 (only SB 253).

Your path to compliance (SB 261)

- Conduct a climate hazard assessment covering both potential physical risks (e.g., wildfire, flooding, extreme heat) and transition risks (e.g., regulation, insurance, carbon pricing). For many companies, this also involves modeling potential scenarios, integrating climate considerations into governance processes, and ensuring board-level oversight—steps that extend beyond disclosure into core business strategy.

- Choose your reporting framework. SB 261 allows alignment with the TCFD framework, the more comprehensive IFRS S2 standards, or another framework prescribed by a government or regulated exchange.

- Draft financial risk disclosures aligned with CARB’s checklist, saving time for internal review and benchmarking against peers if possible.

- Engage internal stakeholders. Finance and legal departments, supply chain managers, and the board all play critical roles. Cross-functional coordination helps ensure climate-risk reporting is accurate, relevant, and integrated into enterprise-wide risk management, rather than siloed in sustainability teams.

- Engage external experts to support in identifying data gaps, aligning with recognized frameworks, and strengthening your company’s compliance strategy. Working with consultants can help ensure your report not only avoids regulatory risk but also builds credibility with investors.

- Deadlines and fees:

- Prepare to report on the website by January 1, 2026

- Register with CARB’s public docket by July 1, 2026 (opens December 1, 2025)

- Pay the CARB compliance fee of approximately USD 1,403 annually

- Create a strategy to fill disclosure gaps in time for the 2028 submission (i.e., biennial reporting schedule)

SB 261 disclosure process overview

SB 253 and GHG emissions: The next wave

SB 253 disclosures are due starting in 2026:

- Scope 1 and 2 GHG emissions starting June 30, 2026 (subject to change)

- Scope 3 GHG emissions starting in 2027, with exact timing and phasing to be set by CARB through the rulemaking process.

Unlike SB 261, SB 253 requires third-party data assurance. Companies must begin with limited assurance for scope 1 and 2 emissions in 2026 and eventually move to reasonable assurance by 2030—the same rigor applied to financial audits. For scope 3 emissions, limited assurance will be required by 2030. CARB has also noted it may audit assurance and reporting activities, underscoring the need to build robust systems now.

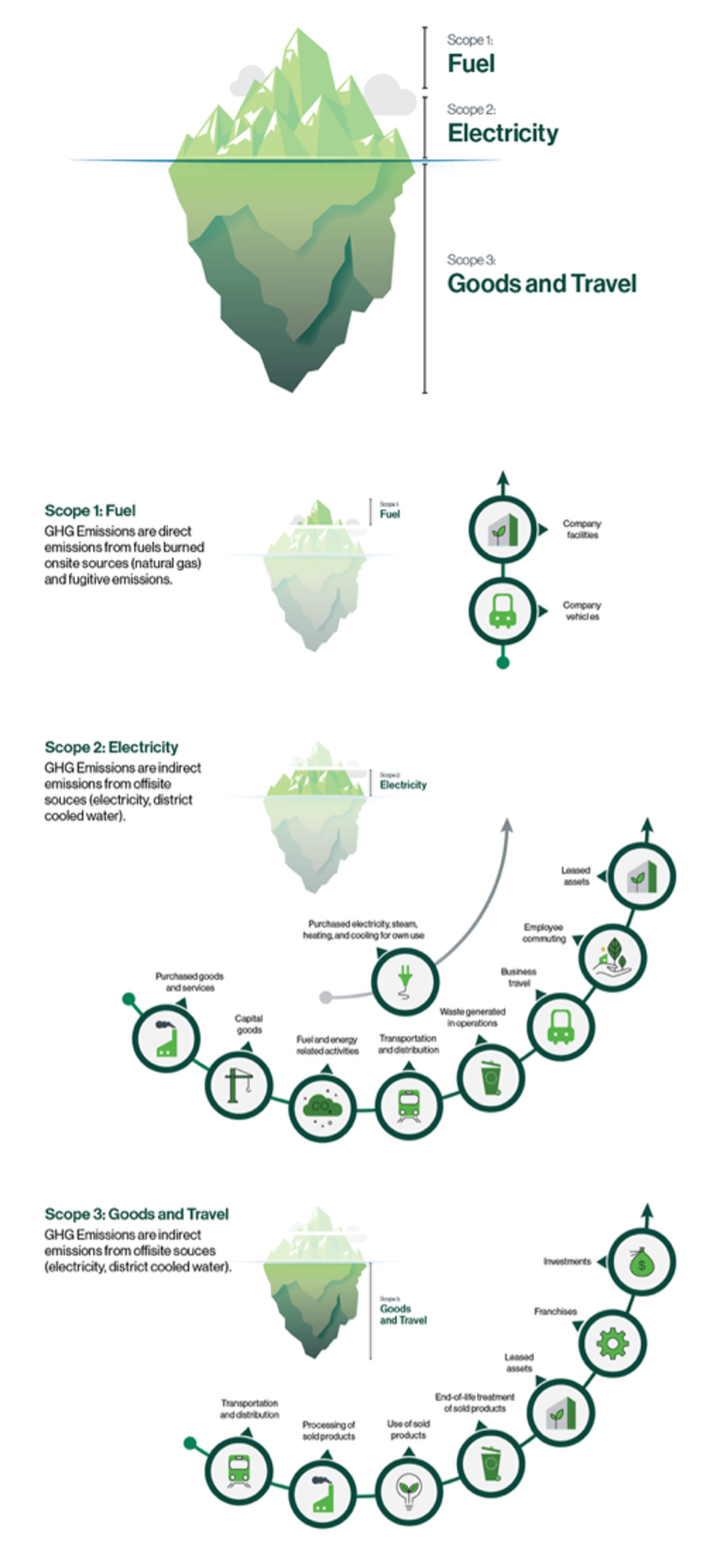

Why Scope 3 is more complex

The biggest challenge for many organizations will be scope 3, or value chain emissions from supply chains, tenant energy use, and construction materials, which often make up the majority of a company’s emissions. Asset management company Robeco reported in 2023 that scope 3 makes up 86% of real estate emissions, seven times more than scopes 1 and 2.

Collecting and validating this data is difficult because it is scattered across suppliers, subsidiaries, and tenants, often requiring a patchwork of utility bills, fuel use records, and third-party estimates where gaps remain.

Your path to compliance (SB 253)

- Check for updates from CARB here. CARB is expected to develop initial rulemaking by Q1 2026.

- Review draft reporting templates for scope 1 and 2 GHG emissions (posted on October 10); CARB is collecting feedback on these templates until October 27 (see link in bullet above to download).

- Review corporate and reporting boundaries to determine what is included in your scope 1 (on-site fuel use) and scope 2 (electricity use) inventories. Assess potential fugitive emissions (a key component of scope 1).

- Review scope 1 and 2 tracking systems for completeness and accuracy.

- Launch a scope 3 materiality assessment to set boundaries and identify data gaps.

- Engage assurance providers in preparation for a capacity crunch as deadlines approach.

- Develop estimation methods and strengthen data gathering systems to support reliable reporting.

- Engage external experts to help assess materiality, compile and verify scope 1–3 emissions data, align reporting with GHG Protocol standards, and prepare for third-party assurance.

- Deadlines and fees:

- Report by June 30, 2026, for scope 1 and 2 emissions (subject to change), with scope 3 reporting requirements phasing in starting in 2027 (subject to change). Data must be assured by a third party.

- Pay the CARB compliance fee of approximately $3,106 annually.

- Create a strategy to fill disclosure gaps in time for the 2027 submission (i.e., annual reporting schedule)

For more background on these laws, see our May 2025 fact sheet, Understanding California’s Climate Legislation—What You Need to Know About SB 253 and SB 261.

Resources

- CARB: Draft Scope 1 and 2 GHG Reporting Template (10/10/2025)

- CARB: Preliminary List of Reporting/Covered Entities and Stakeholder Survey (09/24/2025)

- CARB: Climate Related Financial Disclosures: Draft Checklist (09/02/2025)

- CARB: SB 253/261/219 Public Workshop: Regulation Development and Additional Guidance (08/21/2025)

- CARB: California Corporate Greenhouse Gas Reporting and Climate-Related Financial Risk Disclosure Programs: Frequently Asked Questions Related to Regulatory Development and Initial Reports (07/09/2025)

- Verdani Fact Sheet: Understanding California’s Climate Legislation: What You Need to Know About SB 253 and SB 261 (05/05/2025)

This article was written by Carli Schoenleber,Senior Communications Manager, Content and Engagement Specialist and Paulynn Cue, Chief Communications Officer at Verdani Partners. Learn more about Verdani Partners here.